*Please note that due to NDA restrictions of upcoming unreleased features, the full experience cannot be shown here. Please contact me for a complete demonstration.

*Please note that due to NDA restrictions of upcoming unreleased features, the full experience cannot be shown here. Please contact me for a complete demonstration.

*Please note that due to NDA restrictions of upcoming unreleased features, the full experience cannot be shown here. Please contact me for a complete demonstration.

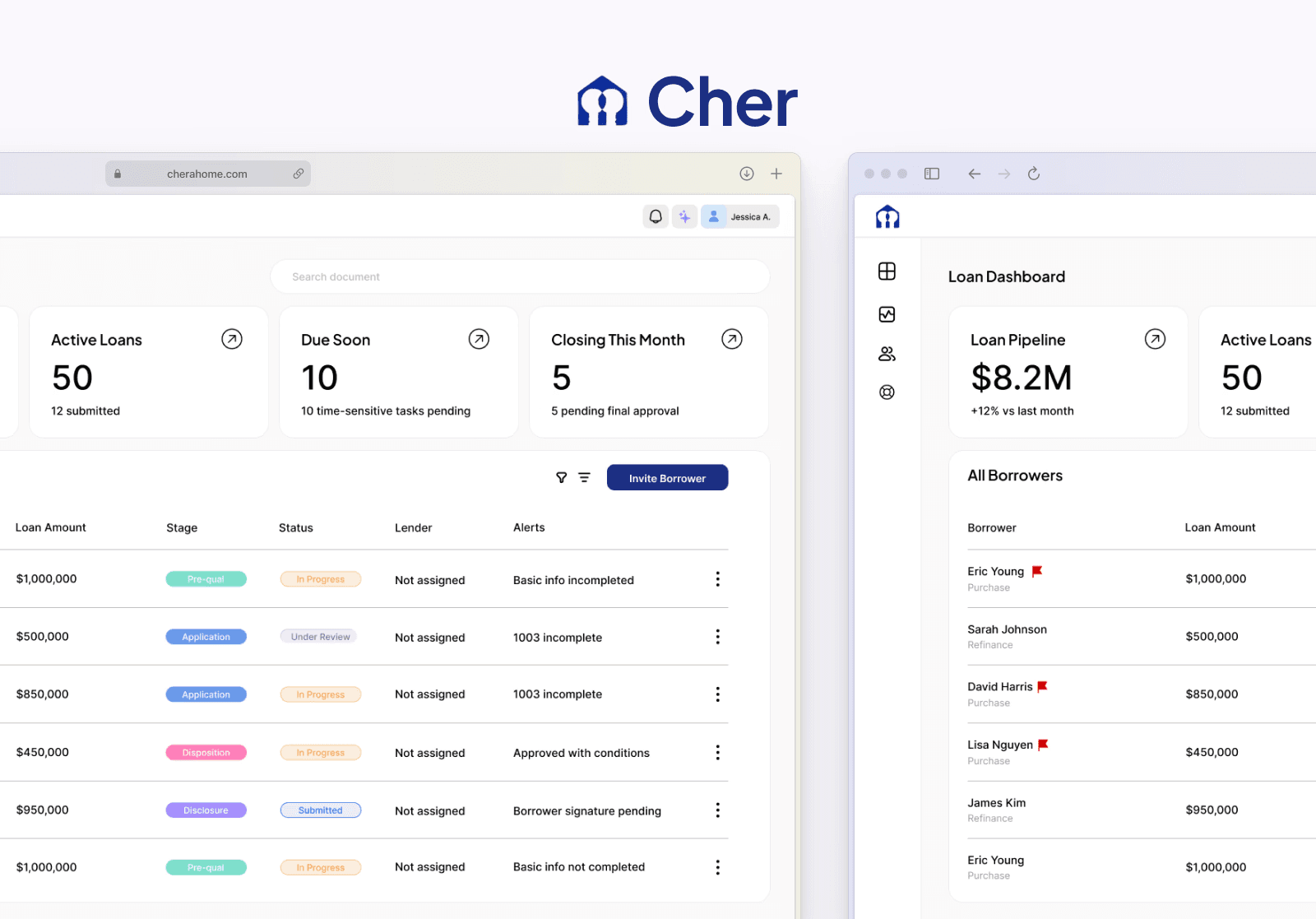

Cher

Cher

Cher

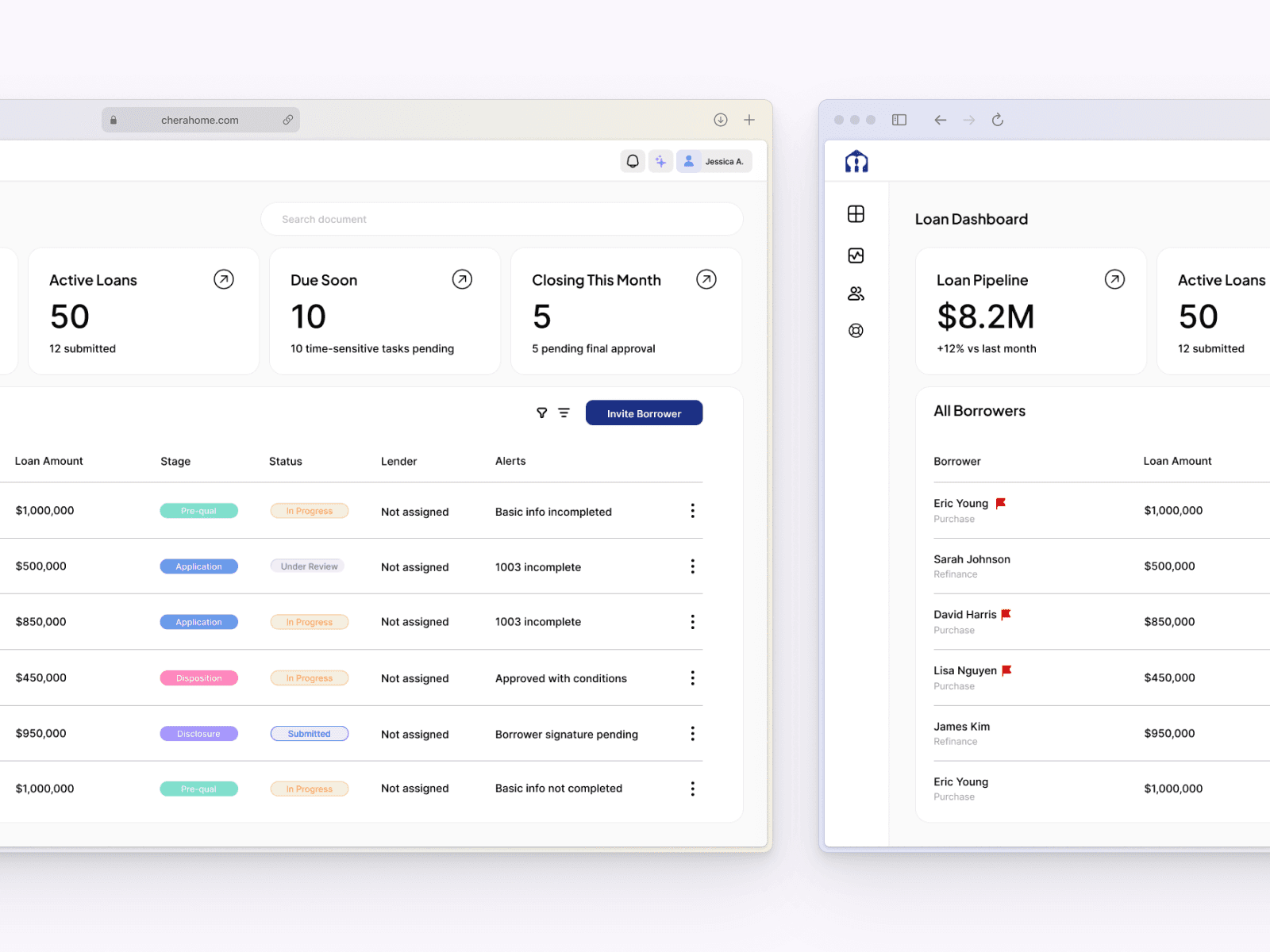

A centralized mortgage platform that streamlines loan workflows for borrowers and loan officers.

A centralized mortgage platform that streamlines loan workflows for borrowers and loan officers.

A centralized mortgage platform that streamlines loan workflows for borrowers and loan officers.

Team

Team

Designers, Engineer, Leadership, Mortgage Team

Designers, Engineer, Leadership, Mortgage Team

Designers, Engineer, Leadership, Mortgage Team

timeline

timeline

Ongoing

Ongoing

Ongoing

Cher

Reducing loan officer workload through a connected mortgage workflow.

✧ What if mortgage workflows felt less fragmented and more collaborative between loan officers and borrowers?

✧ What if mortgage workflows felt less fragmented and more collaborative between loan officers and borrowers?

✧ What if mortgage workflows felt less fragmented and more collaborative between loan officers and borrowers?

Mortgage workflows are often managed across disconnected emails, PDFs, spreadsheets, and manual follow-ups, making collaboration difficult for both borrowers and loan officers.

Mortgage workflows are often fragmented across emails, PDFs, spreadsheets, and manual follow-ups, making it difficult for borrowers and loan officers to stay aligned.

Mortgage workflows are often managed across disconnected emails, PDFs, spreadsheets, and manual follow-ups, making collaboration difficult for both borrowers and loan officers.

Cher centralizes onboarding, document collection, and underwriting preparation into a shared workflow experience designed to reduce repetitive administrative tasks and improve visibility throughout the loan process.

Cher centralizes onboarding, document collection, and underwriting preparation into one shared workflow to reduce admin work and improve loan visibility.

Cher centralizes onboarding, document collection, and underwriting preparation into a shared workflow experience designed to reduce repetitive administrative tasks and improve visibility throughout the loan process.

✧ My Role

✧ My Role

✧ My Role

Led workflow strategy, information architecture, and product design for a mortgage platform focused on reducing operational friction before lender submission.

I led workflow strategy, information architecture, and product design for a mortgage platform focused on reducing operational friction before lender submission.

Led workflow strategy, information architecture, and product design for a mortgage platform focused on reducing operational friction before lender submission.

I translated complex mortgage operations into structured digital workflows by designing onboarding, document collection, underwriting preparation, and AI-assisted verification experiences for both borrowers and loan officers.

I designed borrower and loan officer workflows across onboarding, document collection, underwriting prep, and AI-assisted verification.

I translated complex mortgage operations into structured digital workflows by designing onboarding, document collection, underwriting preparation, and AI-assisted verification experiences for both borrowers and loan officers.

✧ Goals

Creating a more connected workflow between borrowers and loan officers.

The goal was to simplify the mortgage preparation process by reducing manual follow-ups, fragmented communication, and document management across borrowers and loan officers.

✧ Researches & Discovery

Understanding the operational challenges behind the mortgage process.

To better understand the problem space, I conducted stakeholder conversations, workflow observations, and process analysis across key mortgage stages. This helped identify recurring challenges around document collection, underwriting preparation, borrower communication, and workflow visibility.

15 Interviews

Spoke with loan officers and internal stakeholders to understand daily workflows, operational challenges, and existing processes used to manage loans.

5 Workflow Observations

Observed how information moved between borrowers, loan officers, documents, and underwriting workflows to identify areas of friction and coordination gaps.

5 Mortgage Stages Mapped

Mapped the end-to-end mortgage lifecycle to understand handoff points, dependencies, and stages that relied heavily on manual effort.

30+ Artifacts Reviewed

Reviewed existing tools, spreadsheets, document review processes, and communication methods to identify opportunities for consolidation and automation.

Key Insights:

Most operational inefficiencies originated before underwriting began, during borrower onboarding, document collection, and preparation.

✧ What if mortgage workflows felt less fragmented and more collaborative between loan officers and borrowers?

Mortgage workflows are often managed across disconnected emails, PDFs, spreadsheets, and manual follow-ups, making collaboration difficult for both borrowers and loan officers.

Cher centralizes onboarding, document collection, and underwriting preparation into a shared workflow experience designed to reduce repetitive administrative tasks and improve visibility throughout the loan process.

✧ My Role

Led workflow strategy, information architecture, and product design for a mortgage platform focused on reducing operational friction before lender submission.

I translated complex mortgage operations into structured digital workflows by designing onboarding, document collection, underwriting preparation, and AI-assisted verification experiences for both borrowers and loan officers.

✧ Goals

Creating a more connected workflow between borrowers and loan officers.

The goal was to simplify the mortgage preparation process by reducing manual follow-ups, fragmented communication, and document management across borrowers and loan officers.

✧ Researches & Discovery

Understanding the operational challenges behind the mortgage process.

To better understand the problem space, I conducted stakeholder conversations, workflow observations, and process analysis across key mortgage stages. This helped identify recurring challenges around document collection, underwriting preparation, borrower communication, and workflow visibility.

15 Interviews

Spoke with loan officers and internal stakeholders to understand daily workflows, operational challenges, and existing processes used to manage loans.

5 Workflow Observations

Observed how information moved between borrowers, loan officers, documents, and underwriting workflows to identify areas of friction and coordination gaps.

5 Mortgage Stages Mapped

Mapped the end-to-end mortgage lifecycle to understand handoff points, dependencies, and stages that relied heavily on manual effort.

30+ Artifacts Reviewed

Reviewed existing tools, spreadsheets, document review processes, and communication methods to identify opportunities for consolidation and automation.

Key Insights:

Most operational inefficiencies originated before underwriting began, during borrower onboarding, document collection, and preparation.

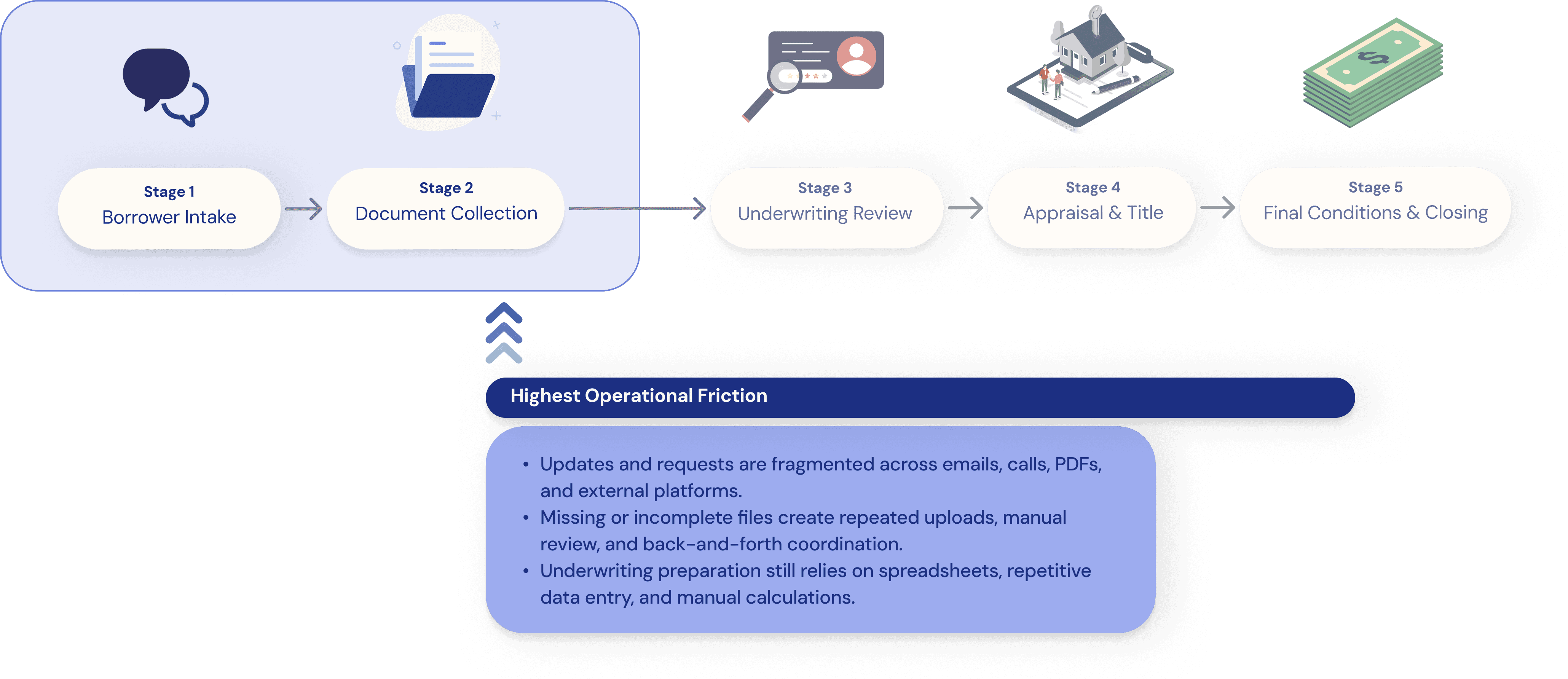

✧ User Journey

Understanding the Loan Officer Journey

Mapping the loan officer journey revealed where manual coordination, borrower follow-ups, and submission readiness created the greatest operational friction throughout the mortgage preparation process. Understanding these challenges helped identify opportunities to streamline workflows, improve visibility, and reduce repetitive administrative work.

Highest Friction

Key Insights:

While the project initially focused on loan officer workflows, many operational delays originated from borrower-side friction, including incomplete applications, missing documents, and repeated follow-ups. This led to designing a connected experience for both borrowers and loan officers.

✧ Goals

✧ Goals

✧ Goals

Creating a more connected workflow between borrowers and loan officers.

Creating a more connected mortgage workflow.

Creating a more connected workflow between borrowers and loan officers.

The goal was to simplify the mortgage preparation process by reducing manual follow-ups, fragmented communication, and document management across borrowers and loan officers.

Reduce manual follow-ups, fragmented communication, and document management by centralizing the experience for borrowers and loan officers.

The goal was to simplify the mortgage preparation process by reducing manual follow-ups, fragmented communication, and document management across borrowers and loan officers.

Through workflow mapping, operational analysis, and user journey exploration, I identified that document collection and underwriting preparation were the stages where repetitive coordination, fragmented communication, and manual workflows most commonly created operational bottlenecks.

✧ Identifying Workflow Bottlenecks

Most operational friction occurred before lender submission.

The goal was to simplify the mortgage preparation process by reducing manual follow-ups, fragmented communication, and document management across borrowers and loan officers.

Through workflow mapping, operational analysis, and user journey exploration, I identified that document collection and underwriting preparation were the stages where repetitive coordination, fragmented communication, and manual workflows most commonly created operational bottlenecks.

✧ System Architecture

Structuring the product around two connected workflows.

The system architecture was designed to connect the borrower-facing application flow with the loan officer workspace. By mapping how information moves from borrower input to loan review, I structured the platform around shared data, document management, underwriting preparation, and activity tracking.

✧ Solution Strategy

Focusing the platform on the stages where operational friction was highest.

Research revealed that the greatest inefficiencies occurred before lender submission, where borrowers and loan officers relied on fragmented communication, manual follow-ups, and document-heavy workflows. Rather than redesigning the entire mortgage lifecycle, I focused the product on borrower onboarding, document collection, and underwriting preparation to reduce coordination overhead and improve loan readiness.

Key Strategic Decision: Focus on pre-lender workflows where coordination, visibility, and document readiness had the greatest impact on loan officer efficiency.

✧ Why This Strategy?

Focusing on the pre-lender stages allowed the platform to address the areas where borrowers and loan officers experienced the highest operational friction throughout the mortgage process.

Rather than focusing on downstream lender or closing workflows, I chose this core framework for three strategic reasons:

Highest Operational Friction

Borrower onboarding, document collection, and underwriting preparation involved the most fragmented communication, repetitive follow-ups, and manual coordination across the mortgage process.

Shared Workflow Dependency

Both borrowers and loan officers rely heavily on each other during the pre-lender stages, making visibility, collaboration, and task coordination critical to loan readiness.

Opportunity for Workflow Simplification

Traditional mortgage preparation workflows still depend on spreadsheets, PDFs, and manual document review, creating opportunities to simplify onboarding, verification, and underwriting preparation through connected digital workflows.

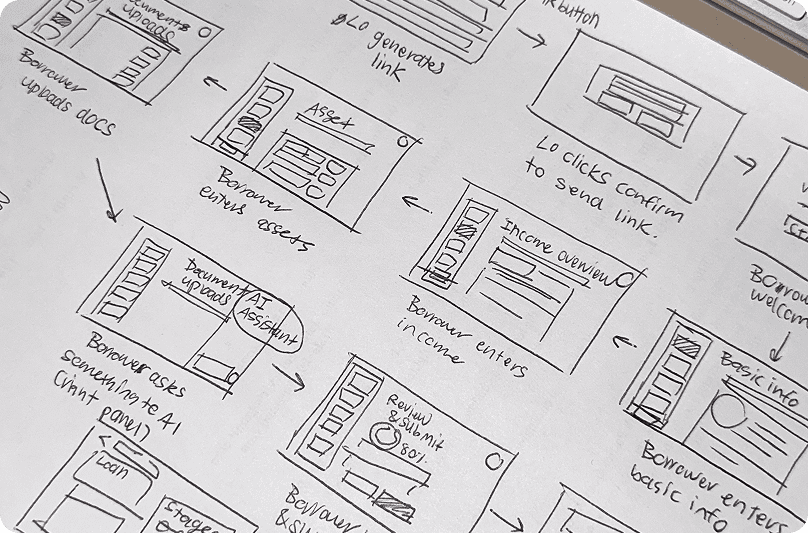

✧ Brainstorm

Exploring how a fragmented mortgage workflow could become a unified experience.

Early ideation focused on identifying opportunities to reduce operational friction across the mortgage process. Rather than designing isolated features, I explored how borrowers, loan officers, documents, underwriting workflows, and communication could be connected through a centralized system.

Workflow Command Center

Create a centralized workspace that helps loan officers manage borrowers, documents, tasks, and underwriting preparation from a single dashboard.

AI Mortgage Assistant

Use AI to analyze uploaded documents, surface risks, explain lender requirements, and guide users through loan preparation.

Connected Collaboration Platform

Create a shared workflow where borrowers and loan officers work from the same source of truth throughout onboarding, document collection, and underwriting preparation.

3 Concepts Explored:

Selected Direction:

Borrowers and loan officers depend on each other throughout the preparation process, making a shared workflow more valuable than isolated borrower or loan officer tools.

✧ Iterations

Validating workflow decisions through stakeholder feedback and usability reviews.

Throughout the design process, I reviewed concepts with stakeholders and tested key workflows against real mortgage preparation tasks. Feedback helped clarify where borrowers needed more guidance, where loan officers needed better visibility, and where automation needed human review before moving files forward.

Clearer next steps for borrowers

Early flows made it difficult for borrowers to understand missing requirements and next actions. I added guided onboarding, progress tracking, and clearer document requirements to reduce confusion and follow-ups.

Loan officers needs faster context

Loan officers needed a quick view of borrower status, outstanding conditions, and loan readiness. I introduced a centralized workspace with action items, status indicators, and key loan metrics.

AI extraction needs human verification

AI-assisted extraction reduced manual entry, but loan officers still needed to verify accuracy. I explored side-by-side review, editable fields, and approval states before data moved forward.

Review needs more confidence

Loan officers needed confidence that a file was ready before submission. I added readiness checks, validation states, and missing-item indicators to reduce rework and improve review efficiency.

Process

✴︎ Borrower Experience

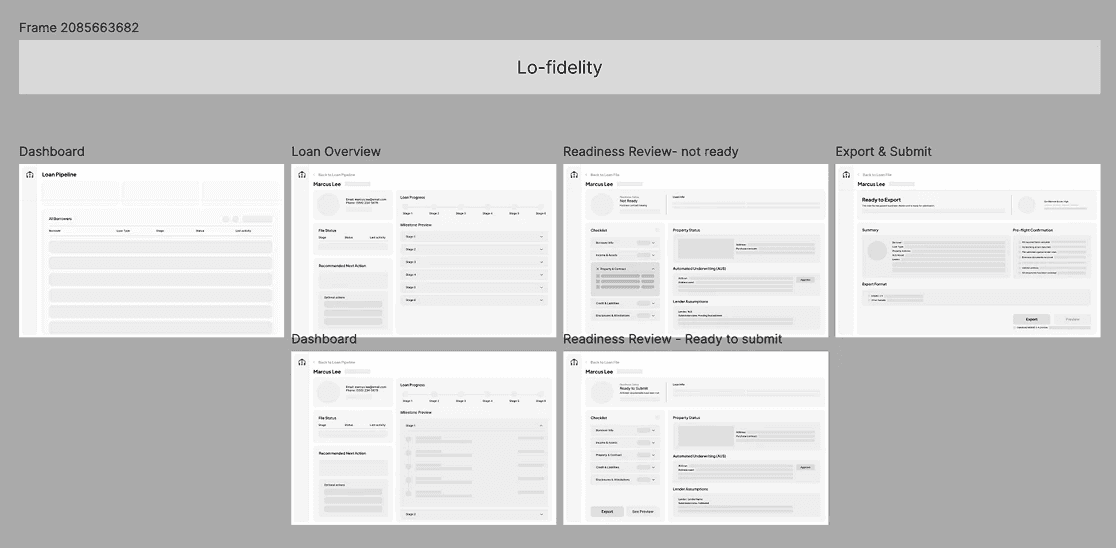

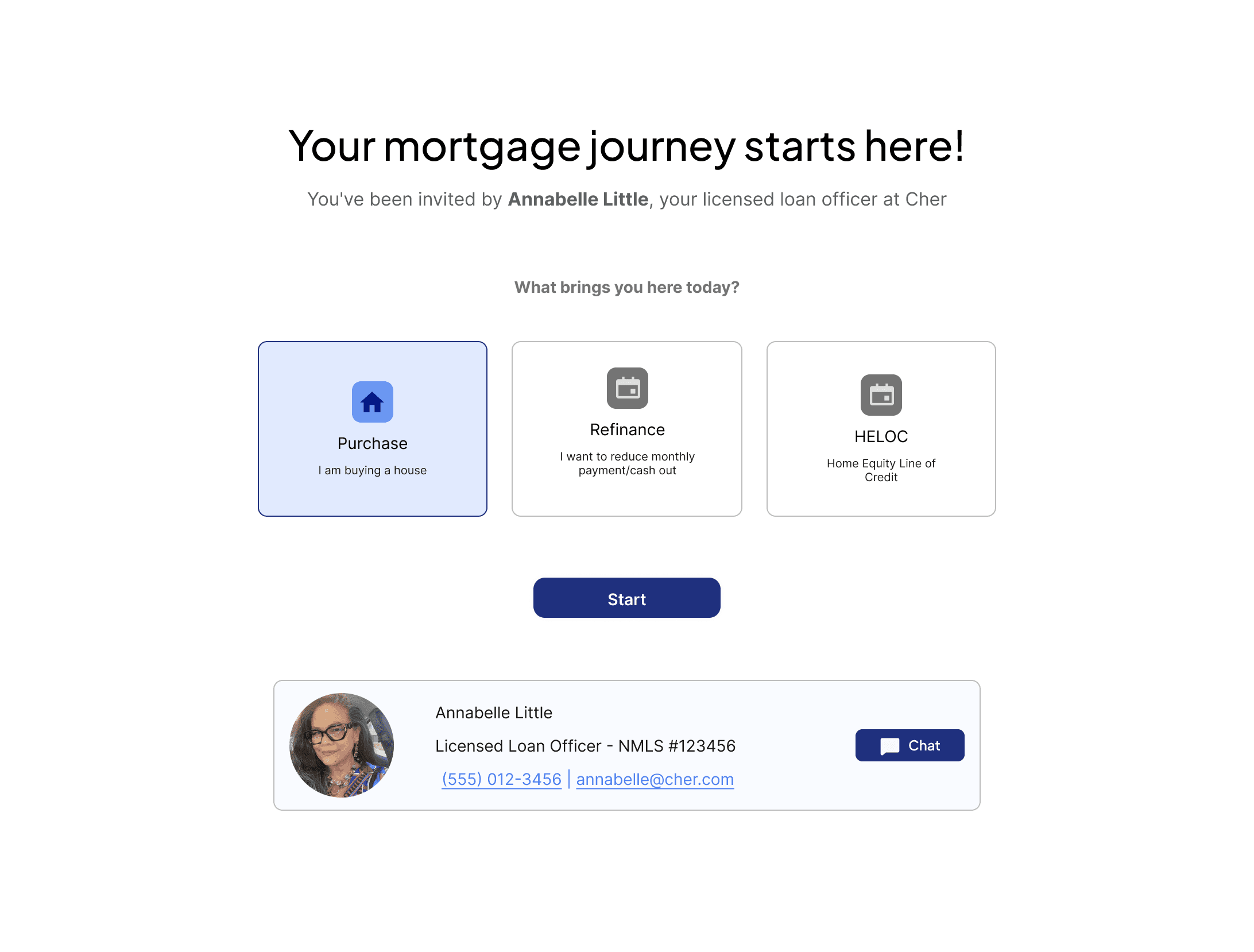

Replaced static mortgage forms with a guided onboarding flow that reduced uncertainty and helped borrowers understand next steps.

Instead of relying on fragmented communication and disconnected forms, the experience transforms the traditional 1003 mortgage application into a structured step-by-step workflow for onboarding, financial information entry, pre-qualification, and document submission.

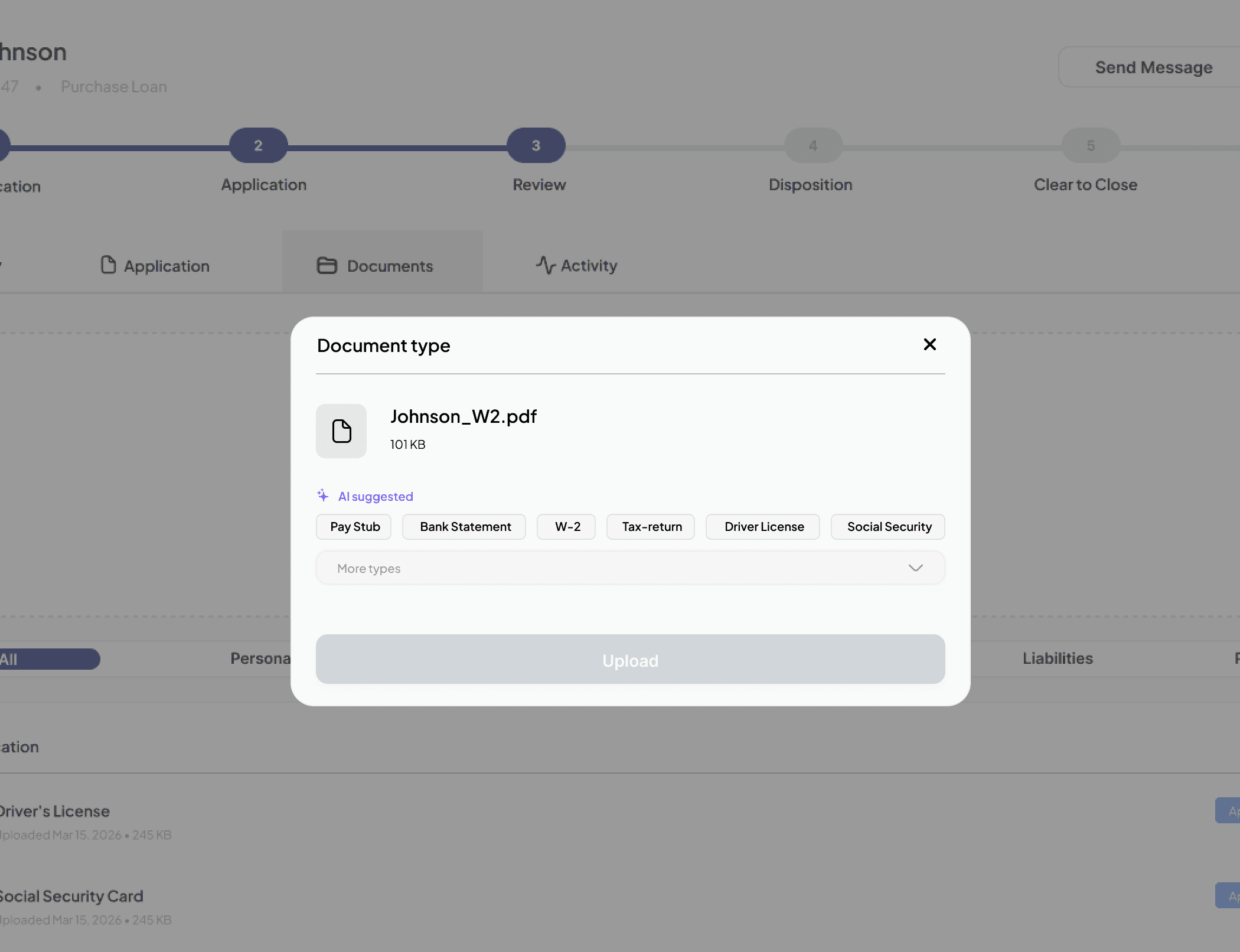

AI-assisted extraction workflows help reduce repetitive manual entry while giving borrowers clearer visibility into outstanding requirements, next steps, and overall loan progress before submission to the loan officer.

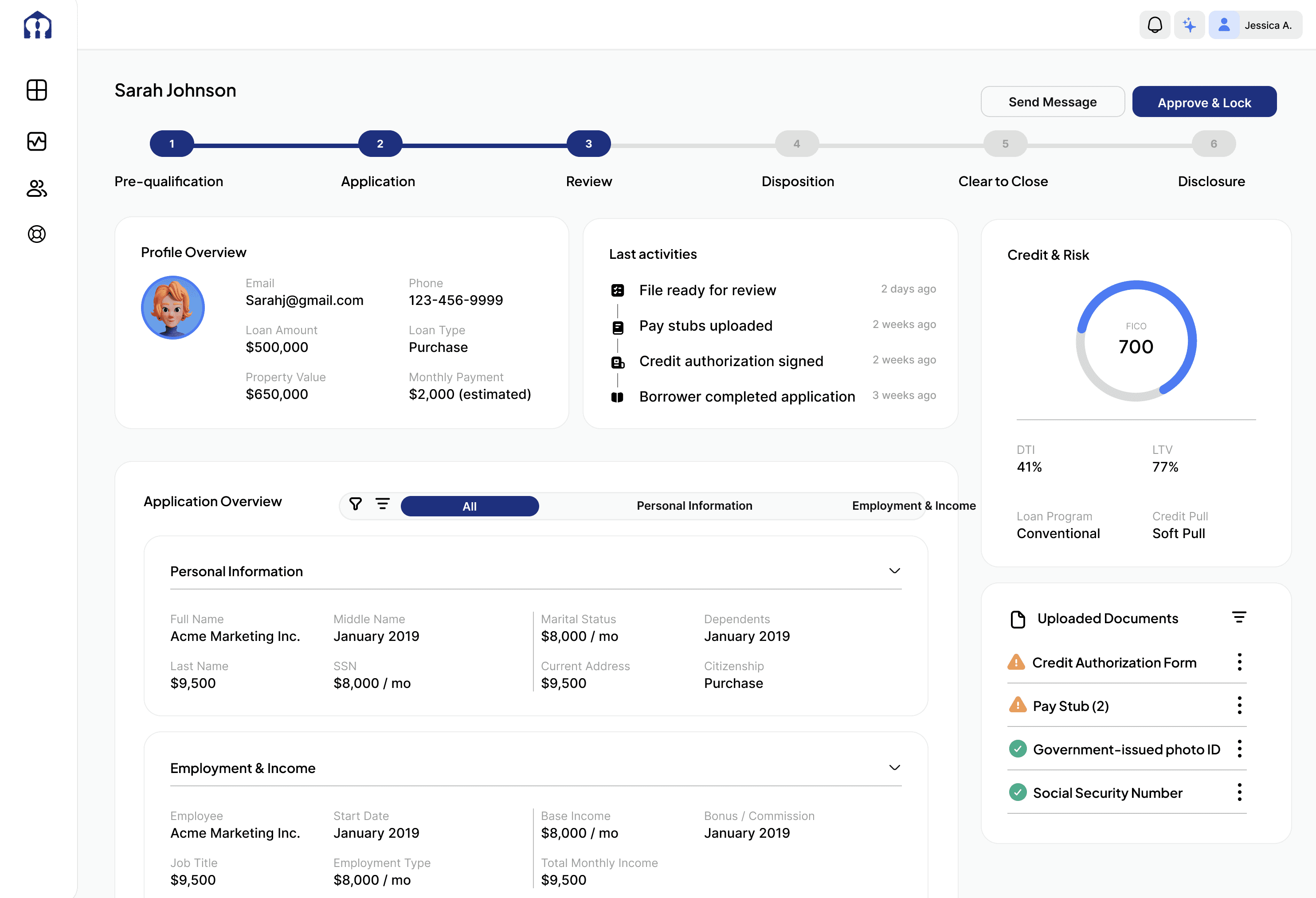

✴︎ Loan Officer Experience

Supporting document review, underwriting preparation, and operational coordination workflows for loan officers.

Once borrowers submit their application, loan officers transition into a centralized workspace for reviewing borrower information, managing outstanding conditions, verifying documents, and preparing loan files for underwriting.

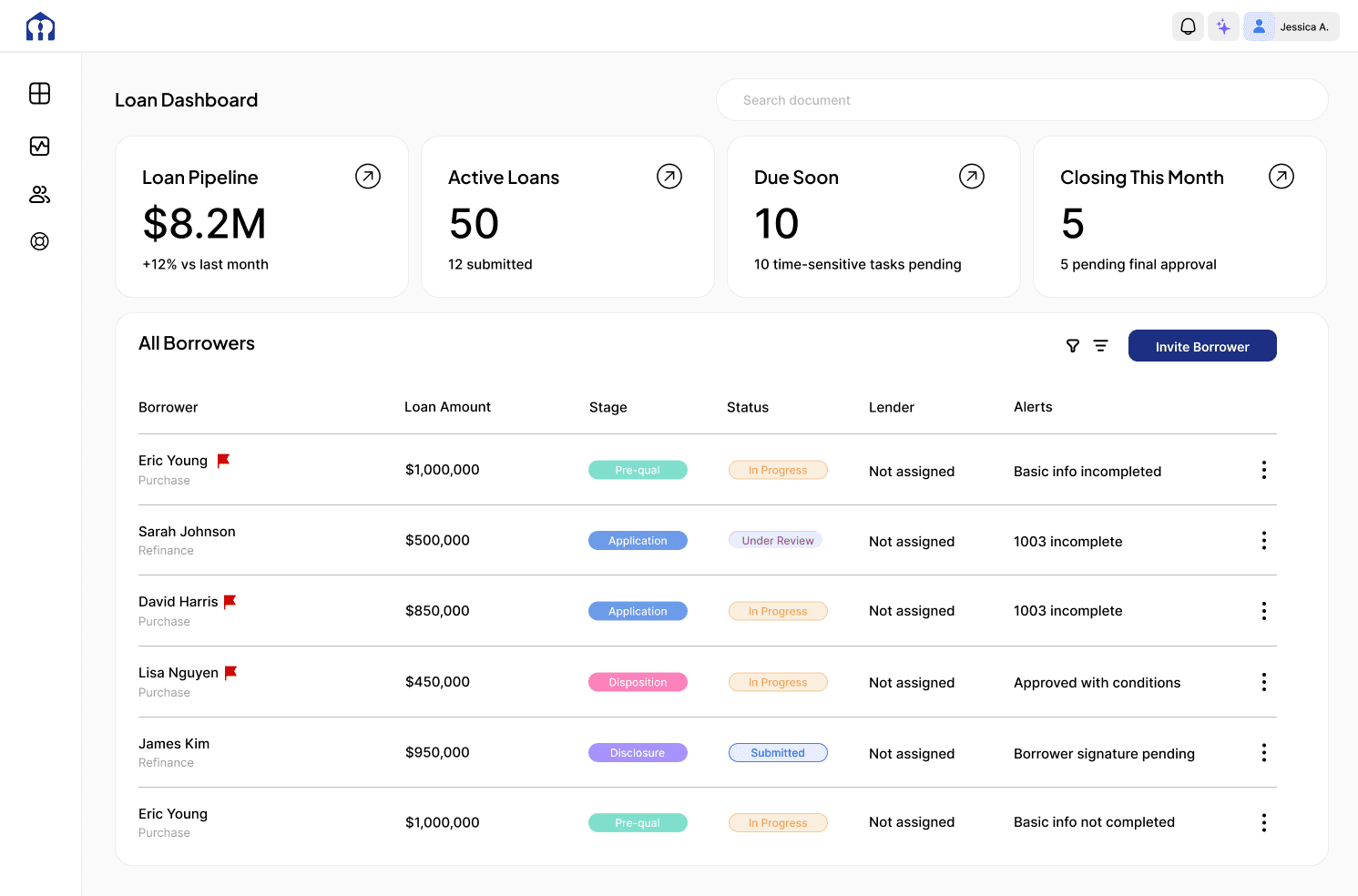

Pipeline Visibility

Challenge

Loan officers had to monitor multiple borrowers while tracking outstanding conditions across fragmented tools.

Solution

Created a centralized dashboard that surfaces borrower status, workflow stage, and outstanding action items in one workspace.

Impact

Reduced context switching and helped loan officers prioritize the highest-priority files.

Document Readiness

Challenge

Document requests and reviews created repeated back-and-forth communication.

Solution

Organized uploaded and missing documents into a structured review workflow with verification states.

Impact

Made document readiness easier to assess and reduced manual coordination.

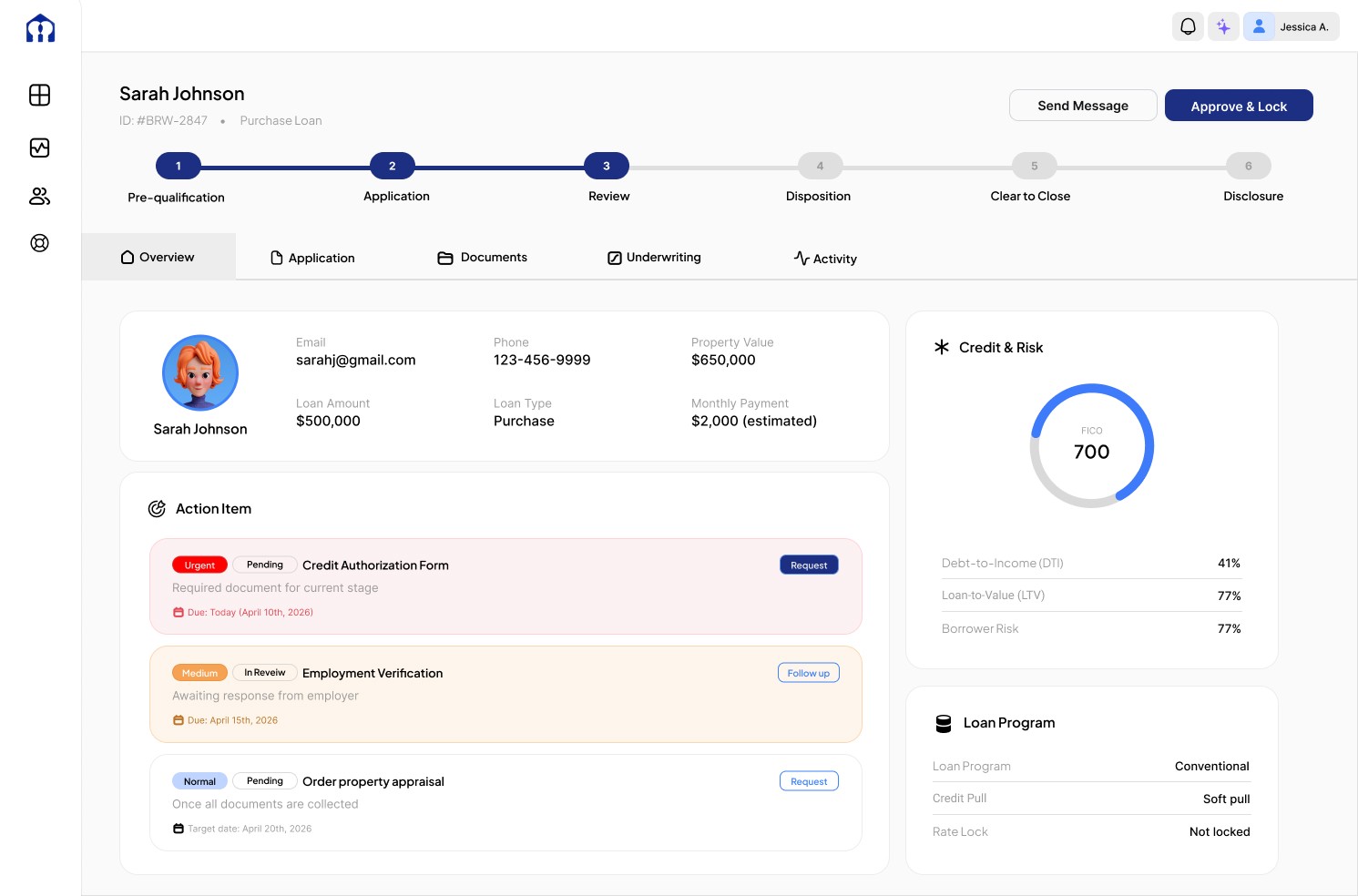

Underwriting Preperation

Challenge

Preparing loan files for underwriting relied heavily on spreadsheets, manual calculations, and document reviews.

Solution

Created a centralized underwriting workspace that combines financial summaries, qualifying income calculations, document verification, and readiness indicators.

Verification Tracking

Reduced manual preparation work and improved confidence before lender submission.

Loan Command Center

Challenge

Critical borrower information was spread across documents, spreadsheets, and communication threads.

Solution

Consolidated borrower details, loan health metrics, and outstanding conditions into a single operational workspace.

Impact

Improved visibility and reduced time spent gathering information before review.

✧ Technial Constraints / Problem Solving

Balancing automation, accuracy, and operational complexity.

Designing for mortgage workflows required navigating constraints around data accuracy, workflow ownership, and system complexity. The challenge was not only creating efficient experiences, but ensuring that automation and visibility supported existing operational processes without reducing trust or control.

AI Extraction vs Human Verification

While AI could reduce manual data entry, loan officers still needed the ability to review, edit, and approve extracted information before it entered the loan workflow.

Info Density vs Usability

Mortgage applications contain large amounts of financial and document data. The experience was structured around progressive disclosure to surface critical information without overwhelming users.

Automation vs Operational Control

Many repetitive tasks could be automated, but key decisions still required human oversight. The solution focused on assisting loan officers rather than replacing existing review processes.

Borrower Simplicity VS Operational Complexity

Loan preparation requires large amounts of financial and document data, but presenting that complexity directly to borrowers would increase friction. The experience was structured to simplify data collection while maintaining the detail needed for loan officer review and underwriting preparation.

Borrower Experience

Guides borrowers through onboarding, pre-qualification, document uploads, and loan preparation through a step-by-step flow.

Loan Officer Experience

Supports loan review, verification, underwriting preparation, and workflow coordination through a centralized operational workspace.

✧ Success Metrics

Measuring the impact of a more connected mortgage workflow.

The proposed solution focuses on reducing operational inefficiencies throughout the mortgage lifecycle by improving visibility, centralizing workflows, and streamlining underwriting preparation. Success would be measured through both workflow efficiency and user adoption metrics.

Reduction in borrower follow-ups

Decrease time spent on borrower follow-ups, status updates, and document requests through centralized workflow management.

Faster document readiness

Increase document completion and approval rates by providing clearer visibility into missing requirements and review status.

Underwriting preparation efficiency

Reduce time spent organizing financial information, reviewing documents, and preparing loans for underwriting submission.

Workflow Transparency

Improve visibility into loan progress, outstanding conditions, and next steps for both borrowers and loan officers.

✧ Learnings

Designing systems requires understanding workflows before interfaces.

Process Before Interface

Mapping the mortgage workflow revealed that many challenges stemmed from operational handoffs, fragmented communication, and disconnected processes rather than individual interface issues.

Visibility Drives Efficiency

Clear ownership, status visibility, and next-step guidance play a critical role in reducing workflow delays and improving coordination between borrowers and loan officers.

Enterprise Products Require Systems Thinking

Designing for complex workflows requires balancing multiple users, business processes, and technical constraints while using AI to support decision-making rather than replace it.

✧ Future Opportunities

Expanding the platform beyond workflow management.

While the current experience focuses on borrower collaboration and underwriting preparation, future iterations could further automate operational processes and provide deeper insights throughout the mortgage lifecycle.

Borrower Engagement & Marketing Tools

Enable loan officers to send personalized updates, educational content, milestone notifications, and follow-up campaigns to borrowers throughout the loan journey, improving communication, transparency, and long-term client relationships.

Workflow Automation & AI Assistance

Expand automation capabilities through intelligent task management, document analysis, underwriting support, and proactive workflow recommendations to reduce manual effort across the mortgage process.

✴︎ Outcome

The final solution transformed fragmented borrower onboarding, document collection, and underwriting preparation into a shared workflow that improved visibility and reduced manual coordination before lender submission.

Cher explored how centralized workflows, guided onboarding, and AI-assisted verification could reduce operational friction during mortgage preparation. By restructuring fragmented document collection and underwriting preparation workflows into a shared platform, the experience helps improve visibility, reduce repetitive manual coordination, and support clearer collaboration throughout the loan process.

✧ Researches & Discovery

✧ Researches & Discovery

Understanding the operational challenges behind the mortgage process.

Understanding the operational challenges behind the mortgage process.

Understanding the operational challenges behind the mortgage process.

To better understand the problem space, I conducted stakeholder conversations, workflow observations, and process analysis across key mortgage stages. This helped identify recurring challenges around document collection, underwriting preparation, borrower communication, and workflow visibility.

Research focused on understanding operational workflows, stakeholder needs, and coordination challenges across the mortgage process.

To better understand the problem space, I conducted stakeholder conversations, workflow observations, and process analysis across key mortgage stages. This helped identify recurring challenges around document collection, underwriting preparation, borrower communication, and workflow visibility.

15 Interviews

15

15 Interviews

Spoke with loan officers and internal stakeholders to understand daily workflows, operational challenges, and existing processes used to manage loans.

Interviews

Spoke with loan officers and internal stakeholders to understand daily workflows, operational challenges, and existing processes used to manage loans.

5 Workflow Observations

5

5 Workflow Observations

Observed how information moved between borrowers, loan officers, documents, and underwriting workflows to identify areas of friction and coordination gaps.

Workflow Observations

Observed how information moved between borrowers, loan officers, documents, and underwriting workflows to identify areas of friction and coordination gaps.

5 Mortgage Stages Mapped

5

5 Mortgage Stages Mapped

Mapped the end-to-end mortgage lifecycle to understand handoff points, dependencies, and stages that relied heavily on manual effort.

Mortgage Stages Mapped

Mapped the end-to-end mortgage lifecycle to understand handoff points, dependencies, and stages that relied heavily on manual effort.

30+ Artifacts Reviewed

30+

30+ Artifacts Reviewed

Reviewed existing tools, spreadsheets, document review processes, and communication methods to identify opportunities for consolidation and automation.

Artifacts Reviewed

Reviewed existing tools, spreadsheets, document review processes, and communication methods to identify opportunities for consolidation and automation.

Key Insights:

Key Insights:

Key Insights:

Most operational inefficiencies originated before underwriting began, during borrower onboarding, document collection, and preparation.

Most operational friction occurred before underwriting, during borrower onboarding, document collection, and loan preparation.

Most operational inefficiencies originated before underwriting began, during borrower onboarding, document collection, and preparation.

✧ Identifying Workflow Bottlenecks

✧ Identifying Workflow Bottlenecks

Most operational friction occurred before lender submission.

Most operational friction occurred before lender submission.

Most operational friction occurred before lender submission.

Through workflow mapping, operational analysis, and user journey exploration, I identified that document collection and underwriting preparation were the stages where repetitive coordination, fragmented communication, and manual workflows most commonly created operational bottlenecks.

Through workflow mapping, operational analysis, and user journey exploration, I identified that document collection and underwriting preparation were the stages where repetitive coordination, fragmented communication, and manual workflows most commonly created operational bottlenecks.

✧ User Journey

✧ User Journey

Understanding the Loan Officer Journey

Understanding where loan officers spend the most operational effort.

Understanding the Loan Officer Journey

Mapping the loan officer journey revealed where manual coordination, borrower follow-ups, and submission readiness created the greatest operational friction throughout the mortgage preparation process. Understanding these challenges helped identify opportunities to streamline workflows, improve visibility, and reduce repetitive administrative work.

Mapping the end-to-end loan officer journey revealed that borrower follow-ups, document collection, and submission preparation generated the greatest operational friction. These insights guided the design of a more connected workflow.

Highest Friction

Highest Friction

Highest Friction

Key Insights:

Key Insights:

Key Insights:

While the project initially focused on loan officer workflows, many operational delays originated from borrower-side friction, including incomplete applications, missing documents, and repeated follow-ups. This led to designing a connected experience for both borrowers and loan officers.

Although the project began with loan officer workflows, research revealed that many delays originated from borrower-side friction. This shifted the solution toward a connected experience for both users.

While the project initially focused on loan officer workflows, many operational delays originated from borrower-side friction, including incomplete applications, missing documents, and repeated follow-ups. This led to designing a connected experience for both borrowers and loan officers.

✧ System Architecture

✧ System Architecture

Structuring the product around two connected workflows.

Structuring the product around two connected workflows.

Structuring the product around two connected workflows.

The system architecture was designed to connect the borrower-facing application flow with the loan officer workspace. By mapping how information moves from borrower input to loan review, I structured the platform around shared data, document management, underwriting preparation, and activity tracking.

The platform was structured around two connected workflows, allowing borrower information to seamlessly flow into the loan officer workspace for review, document management, and underwriting preparation.

✧ Solution Strategy

✧ Solution Strategy

Focusing the platform on the stages where operational friction was highest.

Designing for the highest-impact workflows first.

Focusing the platform on the stages where operational friction was highest.

Research revealed that the greatest inefficiencies occurred before lender submission, where borrowers and loan officers relied on fragmented communication, manual follow-ups, and document-heavy workflows. Rather than redesigning the entire mortgage lifecycle, I focused the product on borrower onboarding, document collection, and underwriting preparation to reduce coordination overhead and improve loan readiness.

Rather than redesigning the entire mortgage lifecycle, I focused the MVP on borrower onboarding, document collection, and underwriting preparation, where research identified the greatest opportunities to improve coordination and reduce manual work.

Key Strategic Decision: Focus on pre-lender workflows where coordination, visibility, and document readiness had the greatest impact on loan officer efficiency.

✧ Why This Strategy?

✧ Why This Strategy?

Focusing on the pre-lender stages allowed the platform to address the areas where borrowers and loan officers experienced the highest operational friction throughout the mortgage process.

Focusing on the workflows with the greatest operational impact.

Focusing on the pre-lender stages allowed the platform to address the areas where borrowers and loan officers experienced the highest operational friction throughout the mortgage process.

Rather than focusing on downstream lender or closing workflows, I chose this core framework for three strategic reasons:

Research showed the biggest opportunities existed before lender submission, where borrowers and loan officers collaborated most frequently.

Highest Operational Friction

Highest Friction

Highest Operational Friction

Borrower onboarding, document collection, and underwriting preparation involved the most fragmented communication, repetitive follow-ups, and manual coordination across the mortgage process.

Most delays occurred during onboarding, document collection, and underwriting preparation.

Borrower onboarding, document collection, and underwriting preparation involved the most fragmented communication, repetitive follow-ups, and manual coordination across the mortgage process.

Shared Workflow Dependency

Shared Workflow Dependency

Shared Workflow Dependency

Both borrowers and loan officers rely heavily on each other during the pre-lender stages, making visibility, collaboration, and task coordination critical to loan readiness.

Borrowers and loan officers rely on each other to keep loans moving.

Both borrowers and loan officers rely heavily on each other during the pre-lender stages, making visibility, collaboration, and task coordination critical to loan readiness.

Opportunity for Workflow Simplification

Opportunity

Opportunity for Workflow Simplification

Traditional mortgage preparation workflows still depend on spreadsheets, PDFs, and manual document review, creating opportunities to simplify onboarding, verification, and underwriting preparation through connected digital workflows.

Centralizing these workflows reduces manual coordination and improves readiness.

Traditional mortgage preparation workflows still depend on spreadsheets, PDFs, and manual document review, creating opportunities to simplify onboarding, verification, and underwriting preparation through connected digital workflows.

✧ Brainstorm

✧ Brainstorm

Exploring how a fragmented mortgage workflow could become a unified experience.

Exploring how a fragmented mortgage workflow could become a unified experience.

Exploring how a fragmented mortgage workflow could become a unified experience.

Early ideation focused on identifying opportunities to reduce operational friction across the mortgage process. Rather than designing isolated features, I explored how borrowers, loan officers, documents, underwriting workflows, and communication could be connected through a centralized system.

Rather than designing individual features, I explored multiple concepts for connecting borrower and loan officer workflows into a single experience.

3 Concepts Explored:

3 Concepts Explored:

3 Concepts Explored:

Workflow Command Center

Command Center

Workflow Command Center

Create a centralized workspace that helps loan officers manage borrowers, documents, tasks, and underwriting preparation from a single dashboard.

Centralized loan management

Create a centralized workspace that helps loan officers manage borrowers, documents, tasks, and underwriting preparation from a single dashboard.

AI Mortgage Assistant

AI Assistant

AI Mortgage Assistant

Use AI to analyze uploaded documents, surface risks, explain lender requirements, and guide users through loan preparation.

AI-guided document review

Use AI to analyze uploaded documents, surface risks, explain lender requirements, and guide users through loan preparation.

Connected Collaboration Platform

Connected Platform

Connected Collaboration Platform

Create a shared workflow where borrowers and loan officers work from the same source of truth throughout onboarding, document collection, and underwriting preparation.

Shared borrower and LO experience

Create a shared workflow where borrowers and loan officers work from the same source of truth throughout onboarding, document collection, and underwriting preparation.

Selected Direction:

Selected Direction:

Selected Direction:

Borrowers and loan officers depend on each other throughout the preparation process, making a shared workflow more valuable than isolated borrower or loan officer tools.

A connected workflow that keeps borrowers and loan officers working from the same source of truth.

Borrowers and loan officers depend on each other throughout the preparation process, making a shared workflow more valuable than isolated borrower or loan officer tools.

✧ Iterations

✧ Iterations

Validating workflow decisions through stakeholder feedback and usability reviews.

Refining the experience through continuous feedback.

Validating workflow decisions through stakeholder feedback and usability reviews.

Throughout the design process, I reviewed concepts with stakeholders and tested key workflows against real mortgage preparation tasks. Feedback helped clarify where borrowers needed more guidance, where loan officers needed better visibility, and where automation needed human review before moving files forward.

Stakeholder reviews and workflow walkthroughs helped refine navigation, document review, underwriting preparation, and borrower guidance throughout the product.

Clearer next steps for borrowers

Borrower Guidance

Clearer next steps for borrowers

Early flows made it difficult for borrowers to understand missing requirements and next actions. I added guided onboarding, progress tracking, and clearer document requirements to reduce confusion and follow-ups.

Added clearer next steps and document requirements to reduce confusion.

Early flows made it difficult for borrowers to understand missing requirements and next actions. I added guided onboarding, progress tracking, and clearer document requirements to reduce confusion and follow-ups.

Loan officers needs faster context

Loan Officer Visibility

Loan officers needs faster context

Loan officers needed a quick view of borrower status, outstanding conditions, and loan readiness. I introduced a centralized workspace with action items, status indicators, and key loan metrics.

Surfaced action items, loan status, and key metrics in one workspace.

Loan officers needed a quick view of borrower status, outstanding conditions, and loan readiness. I introduced a centralized workspace with action items, status indicators, and key loan metrics.

AI extraction needs human verification

AI Review

AI extraction needs human verification

AI-assisted extraction reduced manual entry, but loan officers still needed to verify accuracy. I explored side-by-side review, editable fields, and approval states before data moved forward.

Combined AI extraction with manual verification to improve trust.

AI-assisted extraction reduced manual entry, but loan officers still needed to verify accuracy. I explored side-by-side review, editable fields, and approval states before data moved forward.

Review needs more confidence

Submission Readiness

Review needs more confidence

Loan officers needed confidence that a file was ready before submission. I added readiness checks, validation states, and missing-item indicators to reduce rework and improve review efficiency.

Introduced readiness indicators before MISMO export.

Loan officers needed confidence that a file was ready before submission. I added readiness checks, validation states, and missing-item indicators to reduce rework and improve review efficiency.

Process

Process

Process

✴︎ Borrower Experience

✴︎ Borrower Experience

Replaced static mortgage forms with a guided onboarding flow that reduced uncertainty and helped borrowers understand next steps.

Replaced static mortgage forms with a guided onboarding experience.

Replaced static mortgage forms with a guided onboarding flow that reduced uncertainty and helped borrowers understand next steps.

Instead of relying on fragmented communication and disconnected forms, the experience transforms the traditional 1003 mortgage application into a structured step-by-step workflow for onboarding, financial information entry, pre-qualification, and document submission.

AI-assisted extraction workflows help reduce repetitive manual entry while giving borrowers clearer visibility into outstanding requirements, next steps, and overall loan progress before submission to the loan officer.

Instead of disconnected forms and manual follow-ups, borrowers complete a guided application that combines onboarding, financial information, document collection, and pre-qualification into one continuous workflow.

AI-assisted extraction reduces manual entry while helping borrowers understand outstanding requirements, next steps, and overall loan readiness before submission.

Instead of relying on fragmented communication and disconnected forms, the experience transforms the traditional 1003 mortgage application into a structured step-by-step workflow for onboarding, financial information entry, pre-qualification, and document submission.

AI-assisted extraction workflows help reduce repetitive manual entry while giving borrowers clearer visibility into outstanding requirements, next steps, and overall loan progress before submission to the loan officer.

✴︎ Loan Officer Experience

✴︎ Loan Officer Experience

Supporting document review, underwriting preparation, and operational coordination workflows for loan officers.

Supporting document review, underwriting preparation, and operational coordination workflows for loan officers.

Supporting document review, underwriting preparation, and operational coordination workflows for loan officers.

Once borrowers submit their application, loan officers transition into a centralized workspace for reviewing borrower information, managing outstanding conditions, verifying documents, and preparing loan files for underwriting.

Once borrowers submit their application, loan officers manage the entire pre-lender workflow from a centralized workspace for reviewing documents, tracking conditions, and preparing loans for underwriting.

Once borrowers submit their application, loan officers transition into a centralized workspace for reviewing borrower information, managing outstanding conditions, verifying documents, and preparing loan files for underwriting.

Pipeline Visibility

Pipeline Visibility

Pipeline Visibility

Challenge

Challenge

Challenge

Loan officers had to monitor multiple borrowers while tracking outstanding conditions across fragmented tools.

Loan officers managed multiple borrowers across fragmented systems.

Loan officers had to monitor multiple borrowers while tracking outstanding conditions across fragmented tools.

Solution

Solution

Solution

Created a centralized dashboard that surfaces borrower status, workflow stage, and outstanding action items in one workspace.

Centralized borrower status, workflow stages, and action items into one dashboard.

Created a centralized dashboard that surfaces borrower status, workflow stage, and outstanding action items in one workspace.

Impact

Outcome

Impact

Reduced context switching and helped loan officers prioritize the highest-priority files.

Improved visibility and reduced context switching.

Reduced context switching and helped loan officers prioritize the highest-priority files.

Loan Command Center

Loan Command Center

Loan Command Center

Challenge

Challenge

Challenge

Critical borrower information was spread across documents, spreadsheets, and communication threads.

Borrower information was scattered across documents, spreadsheets, and communication threads.

Critical borrower information was spread across documents, spreadsheets, and communication threads.

Solution

Solution

Solution

Consolidated borrower details, loan health metrics, and outstanding conditions into a single operational workspace.

Created a unified workspace for borrower details, loan health, and outstanding conditions.

Consolidated borrower details, loan health metrics, and outstanding conditions into a single operational workspace.

Impact

Outcome

Impact

mproved visibility and reduced time spent gathering information before review.

Reduced time spent gathering information before review.

mproved visibility and reduced time spent gathering information before review.

Document Readiness

Document Readiness

Document Readiness

Challenge

Challenge

Challenge

Document requests and reviews created repeated back-and-forth communication.

Document requests and reviews created repeated back-and-forth communication.

Document requests and reviews created repeated back-and-forth communication.

Solution

Solution

Solution

Organized uploaded and missing documents into a structured review workflow with verification states.

Organized uploaded, missing, and verified documents into a single review workflow.

Organized uploaded and missing documents into a structured review workflow with verification states.

Impact

Outcome

Impact

Made document readiness easier to assess and reduced manual coordination.

Reduced manual coordination and improved document readiness.

Made document readiness easier to assess and reduced manual coordination.

Underwriting Preperation

Underwriting Preperation

Underwriting Preperation

Challenge

Challenge

Challenge

Preparing loan files for underwriting relied heavily on spreadsheets, manual calculations, and document reviews.

Preparing loan files for underwriting relied heavily on spreadsheets, manual calculations, and document reviews.

Preparing loan files for underwriting relied heavily on spreadsheets, manual calculations, and document reviews.

Solution

Solution

Solution

Created a centralized underwriting workspace that combines financial summaries, qualifying income calculations, document verification, and readiness indicators.

Centralized qualifying income, financial review, document verification, and submission readiness into one workspace.

Created a centralized underwriting workspace that combines financial summaries, qualifying income calculations, document verification, and readiness indicators.

Verification Tracking

Outcome

Verification Tracking

Reduced manual preparation work and improved confidence before lender submission.

Reduced manual preparation work and improved confidence before lender submission.

Reduced manual preparation work and improved confidence before lender submission.

✧ Technial Constraints / Problem Solving

✧ Technial Constraints / Problem Solving

Balancing automation, accuracy, and operational complexity.

Balancing automation, accuracy, and operational complexity.

Balancing automation, accuracy, and operational complexity.

Designing for mortgage workflows required navigating constraints around data accuracy, workflow ownership, and system complexity. The challenge was not only creating efficient experiences, but ensuring that automation and visibility supported existing operational processes without reducing trust or control.

Designing mortgage workflows required balancing automation, usability, and operational accuracy while maintaining loan officer trust and control.

Designing for mortgage workflows required navigating constraints around data accuracy, workflow ownership, and system complexity. The challenge was not only creating efficient experiences, but ensuring that automation and visibility supported existing operational processes without reducing trust or control.

AI Extraction vs Human Verification

AI vs Human Verification

AI Extraction vs Human Verification

While AI could reduce manual data entry, loan officers still needed the ability to review, edit, and approve extracted information before it entered the loan workflow.

AI extracts information, but loan officers review and approve before it enters the workflow.

While AI could reduce manual data entry, loan officers still needed the ability to review, edit, and approve extracted information before it entered the loan workflow.

Info Density vs Usability

Information Density

Info Density vs Usability

Mortgage applications contain large amounts of financial and document data. The experience was structured around progressive disclosure to surface critical information without overwhelming users.

Progressive disclosure surfaces critical information without overwhelming users.

Mortgage applications contain large amounts of financial and document data. The experience was structured around progressive disclosure to surface critical information without overwhelming users.

Automation vs Operational Control

Automation vs Control

Automation vs Operational Control

Many repetitive tasks could be automated, but key decisions still required human oversight. The solution focused on assisting loan officers rather than replacing existing review processes.

Automation assists repetitive tasks while preserving human decision-making.

Many repetitive tasks could be automated, but key decisions still required human oversight. The solution focused on assisting loan officers rather than replacing existing review processes.

Borrower Simplicity VS Operational Complexity

Borrower Simplicity VS Operational Complexity

Loan preparation requires large amounts of financial and document data, but presenting that complexity directly to borrowers would increase friction. The experience was structured to simplify data collection while maintaining the detail needed for loan officer review and underwriting preparation.

Loan preparation requires large amounts of financial and document data, but presenting that complexity directly to borrowers would increase friction. The experience was structured to simplify data collection while maintaining the detail needed for loan officer review and underwriting preparation.

Borrower Experience

Guides borrowers through onboarding, pre-qualification, and loan preparation through a step-by-step flow.

Loan Officer Experience

Supports loan review, verification, underwriting preparation, and workflow coordination through a centralized operational workspace.

Borrower Experience

Guides borrowers through onboarding, pre-qualification, and loan preparation.

Loan Officer Experience

Streamlines underwriting preparation, loan operations, and communication.

Borrower Experience

Guides borrowers through onboarding, pre-qualification, and loan preparation.

Loan Officer Experience

Streamlines underwriting preparation, loan operations, and communication.

✴︎ Outcome

✴︎ Outcome

The final solution transformed fragmented borrower onboarding, document collection, and underwriting preparation into a shared workflow that improved visibility and reduced manual coordination before lender submission.

Transforming fragmented mortgage preparation into one connected workflow.

The final solution transformed fragmented borrower onboarding, document collection, and underwriting preparation into a shared workflow that improved visibility and reduced manual coordination before lender submission.

Cher explored how centralized workflows, guided onboarding, and AI-assisted verification could reduce operational friction during mortgage preparation. By restructuring fragmented document collection and underwriting preparation workflows into a shared platform, the experience helps improve visibility, reduce repetitive manual coordination, and support clearer collaboration throughout the loan process.

Cher brings borrower onboarding, document collection, and underwriting preparation into a shared experience that improves visibility, reduces manual coordination, and helps loan officers prepare loans more efficiently before lender submission.

Cher explored how centralized workflows, guided onboarding, and AI-assisted verification could reduce operational friction during mortgage preparation. By restructuring fragmented document collection and underwriting preparation workflows into a shared platform, the experience helps improve visibility, reduce repetitive manual coordination, and support clearer collaboration throughout the loan process.

✧ Success Metrics

✧ Success Metrics

Measuring the impact of a more connected mortgage workflow.

Measuring the impact of a more connected mortgage workflow.

Measuring the impact of a more connected mortgage workflow.

The proposed solution focuses on reducing operational inefficiencies throughout the mortgage lifecycle by improving visibility, centralizing workflows, and streamlining underwriting preparation. Success would be measured through both workflow efficiency and user adoption metrics.

Success would be measured by operational efficiency and workflow adoption.

The proposed solution focuses on reducing operational inefficiencies throughout the mortgage lifecycle by improving visibility, centralizing workflows, and streamlining underwriting preparation. Success would be measured through both workflow efficiency and user adoption metrics.

Reduction in borrower follow-ups

Borrower Follow-ups

Reduction in borrower follow-ups

Decrease time spent on borrower follow-ups, status updates, and document requests through centralized workflow management.

Fewer manual reminders and document requests

Decrease time spent on borrower follow-ups, status updates, and document requests through centralized workflow management.

Faster document readiness

Document Readiness

Faster document readiness

Increase document completion and approval rates by providing clearer visibility into missing requirements and review status.

Faster document completion and verification

Increase document completion and approval rates by providing clearer visibility into missing requirements and review status.

Underwriting preparation efficiency

Underwriting Prep

Underwriting preparation efficiency

Reduce time spent organizing financial information, reviewing documents, and preparing loans for underwriting submission.

Less time preparing loan files

Reduce time spent organizing financial information, reviewing documents, and preparing loans for underwriting submission.

Workflow Transparency

Workflow Visibility

Workflow Transparency

Improve visibility into loan progress, outstanding conditions, and next steps for both borrowers and loan officers.

Improved visibility into loan status and outstanding conditions

Improve visibility into loan progress, outstanding conditions, and next steps for both borrowers and loan officers.

✧ Learnings

✧ Learnings

Designing systems requires understanding workflows before interfaces.

Designing systems requires understanding workflows before interfaces.

Designing systems requires understanding workflows before interfaces.

Designing systems requires understanding workflows before interfaces.

Process Before Interface

Process Before Interface

Process Before Interface

Mapping the mortgage workflow revealed that many challenges stemmed from operational handoffs, fragmented communication, and disconnected processes rather than individual interface issues.

Operational challenges were driven more by fragmented workflows than by individual interface problems.

Mapping the mortgage workflow revealed that many challenges stemmed from operational handoffs, fragmented communication, and disconnected processes rather than individual interface issues.

Visibility Drives Efficiency

Visibility Drives Efficiency

Visibility Drives Efficiency

Clear ownership, status visibility, and next-step guidance play a critical role in reducing workflow delays and improving coordination between borrowers and loan officers.

Clear ownership, status visibility, and next steps reduce delays across complex workflows.

Clear ownership, status visibility, and next-step guidance play a critical role in reducing workflow delays and improving coordination between borrowers and loan officers.

Enterprise Products Require Systems Thinking

Systems Thinking

Enterprise Products Require Systems Thinking

Designing for complex workflows requires balancing multiple users, business processes, and technical constraints while using AI to support decision-making rather than replace it.

Enterprise products require balancing users, business processes, and technical constraints while using AI to assist, not replace, human decisions.

Designing for complex workflows requires balancing multiple users, business processes, and technical constraints while using AI to support decision-making rather than replace it.

✧ Future Opportunities

✧ Future Opportunities

Expanding the platform beyond workflow management.

Expanding the platform beyond workflow management.

Expanding the platform beyond workflow management.

While the current experience focuses on borrower collaboration and underwriting preparation, future iterations could further automate operational processes and provide deeper insights throughout the mortgage lifecycle.

Future iterations could expand beyond mortgage preparation through automation, borrower engagement, and AI-powered operational support.

While the current experience focuses on borrower collaboration and underwriting preparation, future iterations could further automate operational processes and provide deeper insights throughout the mortgage lifecycle.

Borrower Engagement & Marketing Tools

Borrower Engagement

Borrower Engagement & Marketing Tools

Enable loan officers to send personalized updates, educational content, milestone notifications, and follow-up campaigns to borrowers throughout the loan journey, improving communication, transparency, and long-term client relationships.

Personalized updates, milestone notifications, and educational campaigns to strengthen borrower communication and long-term relationships.

Enable loan officers to send personalized updates, educational content, milestone notifications, and follow-up campaigns to borrowers throughout the loan journey, improving communication, transparency, and long-term client relationships.

Workflow Automation & AI Assistance

Workflow Automation & AI

Workflow Automation & AI Assistance

Expand automation capabilities through intelligent task management, document analysis, underwriting support, and proactive workflow recommendations to reduce manual effort across the mortgage process.

AI-assisted task management, document analysis, underwriting support, and proactive workflow recommendations.

Expand automation capabilities through intelligent task management, document analysis, underwriting support, and proactive workflow recommendations to reduce manual effort across the mortgage process.

Borrower Experience

Guides borrowers through onboarding,

pre-qualification, and loan preparation.Loan Officer Experience

Streamlines underwriting preparation, loan operations, and communication.

Copyright © 2025 Penny Asawadilockchai. All Rights Reserved.

Copyright © 2025 Penny Asawadilockchai. All Rights Reserved.

Copyright © 2025 Penny Asawadilockchai. All Rights Reserved.